Salaam,

Guess I’m one of those people who kind of knows something but never really pays attention until something happens to remind me how significant a change that thing could make.

Just yesterday, I woke up with a net worth of 3,000 TZS (a dollar and a quarter, maybe). These are the moments when you remember that pile of clothes in the laundry basket and start the treasure hunt through everything with pockets. Sometimes, you might find a coin or two—enough to pay for a Bajaj or Bodaboda to get you where you need to go—and on a lucky day, maybe even a 10K or 5K you completely forgot existed. Yesterday was not one of those days, and you should have seen the disappointment on my face after an unsuccessful money hunt through all my trousers waiting to be washed.

$100 Bill in the Back of My Phone Case:

Amidst the chaos of wondering whether I’d catch the ferry on time and how the day would unfold since I wasn’t expecting any surprise cash from anyone, I stumbled upon a piece of paper that looked different. I picked up my phone, turned it over, removed the cover, and—voila!—a $100 bill that a friend had gifted me on one of my recent trips, stashed on the back of my phone cover. Like many things that wouldn’t have seen the light of day, this $100 bill was lucky to have stayed in such a safe place, hidden behind a boarding pass and a credit card that had barely an FM radio frequency as its balance—a nice way of saying my card was broke, just like me.

Finding money is one thing, but finding a $100 bill? Immediately, my mind started imagining how I’d “chop life” with that money, all the things I could do with the 200K+ I’d get after converting it to local currency. My last memory of leaving home was cheerfully rhyming and dancing on my way to the Bodaboda. That was 10 a.m.; don’t ask me what time I got back or my net worth by then—just know it was a Friday.

Back to What Brought Us Here.

To spend that $100, you need to convert it to TZS, and only banks can do that. Imagine the long walk on a sunny day in Dar, only to arrive at the nearest bank and find the entire floor packed, with long queues and everyone impatiently waiting for their turn. A simple mistake—like accidentally skipping someone in line—could practically start World War III. Finally, I got to the FX counter.

After filling out forms, photocopying my ID, and almost getting into a fight with the teller for serving someone from a different line during my turn, I cheerfully greeted her, hoping to increase my chances of getting served quickly. “Wait a bit,” she replied, stepped outside, returned a minute later, and immediately started tallying some digits on her computer. I guessed she was calculating my worth in TZS after my $100 bill was converted.

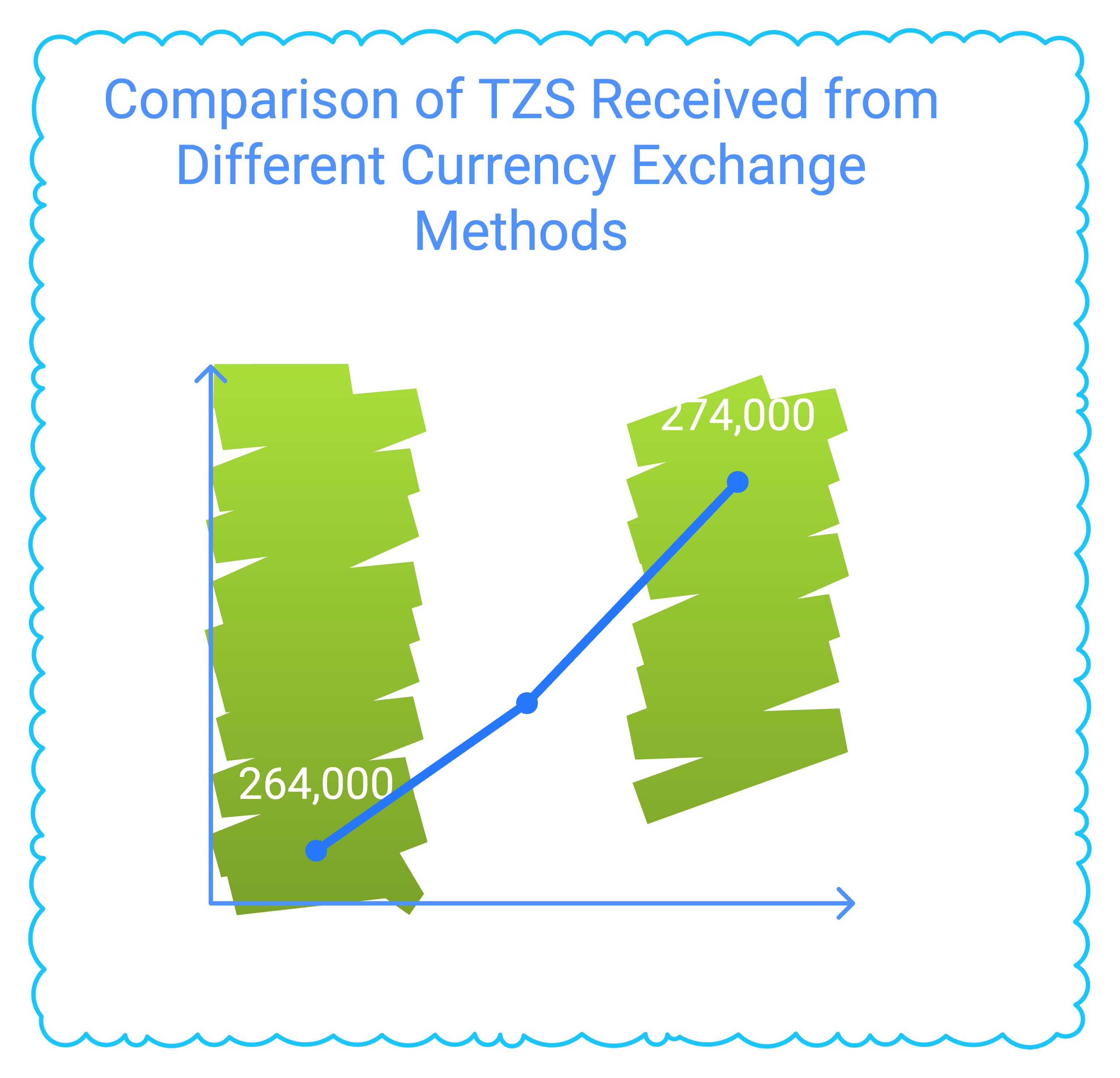

“Sign here,” “sign there,” “here is your money…” She handed me a pile of cash. I eagerly picked it up and started counting right away, only to see my dreams of “chopping life” fade before my eyes. Whaaat? It was 264,000, TZS—4,000 TZS less than what a competitor bank was offering at a rate of 2,680 TZS per dollar, and a whopping 10,000 TZS difference if I’d used a crypto off-ramp at a rate of 2740 TZS.

A Dollar On-Chain: A Dollar Unchained.

Enough with the “get rich quick” thoughts that most people hear when blockchain or crypto is first mentioned. While the majority might think crypto is a fad or a scam with no real use case in Africa, perhaps this $100 bill story will change your mind a little.

Blockchain as a technology and crypto as its application extend beyond get-rich-quick schemes. Looking deeper, crypto, and by extension, Decentralized Finance (DeFi), are engineered to enable money movements, much like traditional financial systems—only with far more flexibility and composability than a typical bank would ever offer. Stablecoins are hands-down the best innovation in the DeFi industry. Imagine a dollar replicated on-chain (a fancy way of saying digitally) that can move freely—unbounded by geography or financial policies imposed by governments—and with additional possibilities for storing wealth, protecting your hard-earned money against inflation, or even working for you by earning higher APYs than any bank could ever promise. Imagine doing all this while maintaining its 1:1 value with an actual dollar, meaning a dollar on-chain can be converted to shillings at the exact rate of a dollar at the counter.

Many, including myself, have always thought having dollars is a safer bet, given how fast TZS and many other African currencies have lost value against the dollar. For smaller economies dependent on dollars to trade with the rest of the world, storing wealth in dollars shields you from abrupt price swings, especially in recent days when prices have skyrocketed.

TradFi: Bad Company Corrupts Good Character

As Passenger famously sang in “Let Her Go”—we never appreciate things until they’re gone. For the first time, I’ve appreciated what 10,000 TZS (nearly 4 dollars) could do. A plate of chicken biryani, a six-pack of my favorite local beers, 5GB of internet—these were a few of the missed opportunities that 10K would have unlocked if only the bank hadn’t robbed me.

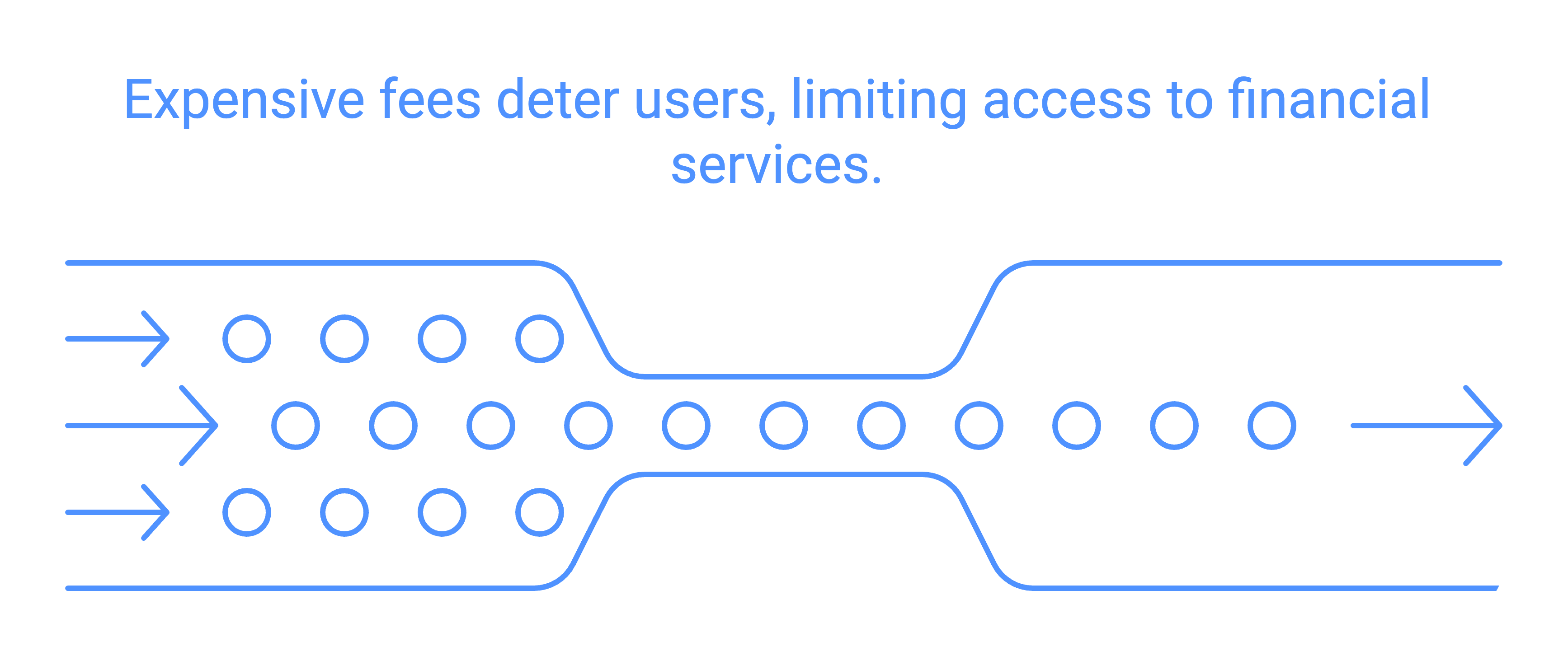

Traditional financial systems, like banks, are a bloodthirsty Frankenstein—built with the core purpose of robbing and siphoning every dollar out of people. For years, this monster has grown and flourished, nourished with pennies stolen from expensive transaction fees, high-interest loans, and, in my case, exploitative FX rates that robbed me of the fun of enjoying my 10,000 TZS.

The crookedness and exploitation of these banks couldn’t have been clearer to me than yesterday. In that moment, I realized that while a dollar might protect you from inflation, that security is rarely a reality when it’s held in fiat (traditional financial systems). This very system erodes even marginal FX differences that could have helped cover inflation costs. Add to that an unregulated rate system, where any bank can set rates based on how greedy they feel. My $100 was exchanged at 2,640, but a competitor bank would have offered me 2,680—a 4K difference. Banks make nearly 10–15K in profit when they resell that $100 bill to someone exchanging TZS to USD. Perhaps this is why so many Tanzanians remain unbanked; in a cost-conscious market like ours, expensive transaction fees, not to mention government levies, have rendered these systems useless for the masses.

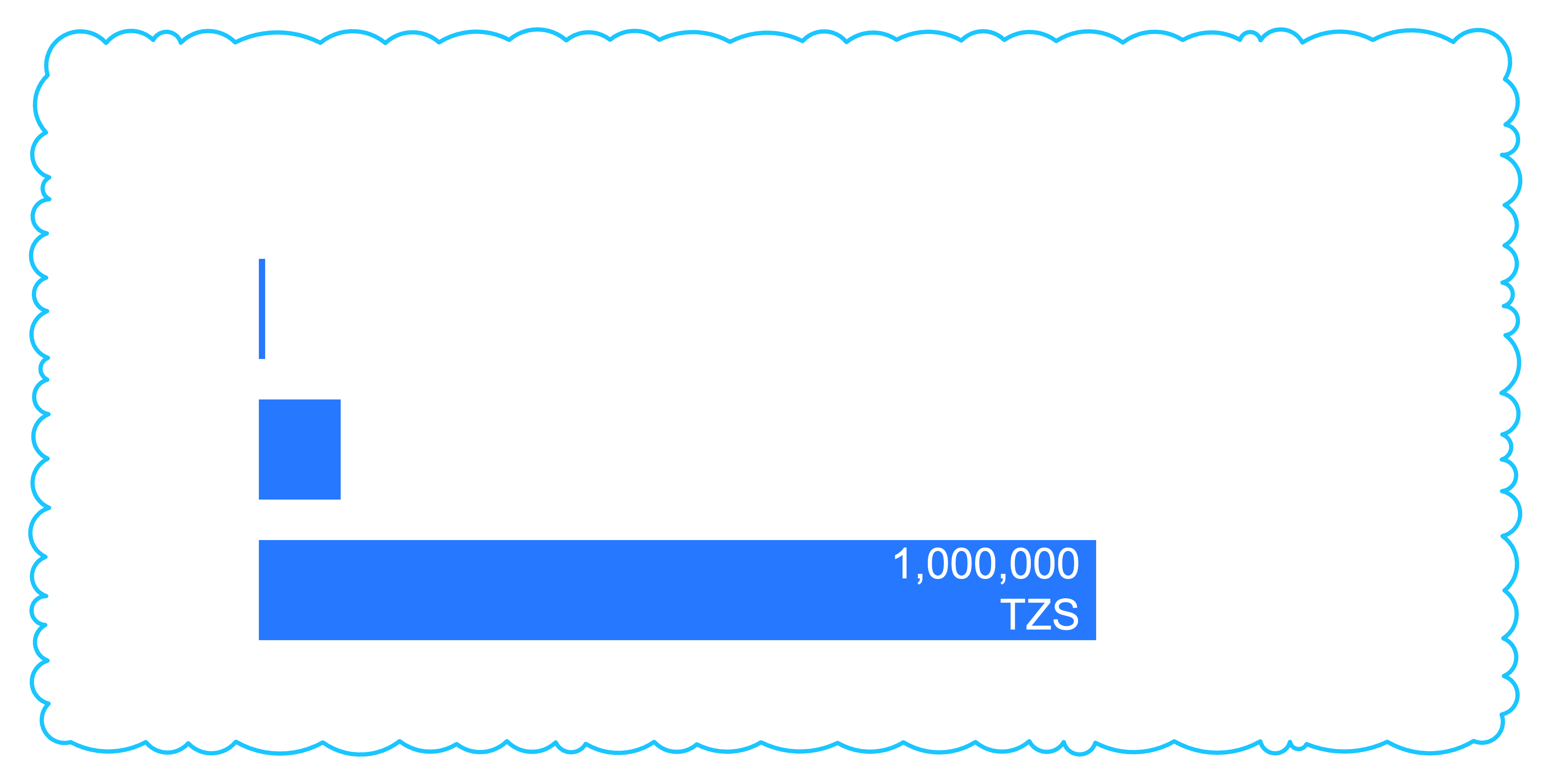

What may seem like a mere 10,000 TZS at first glance can grow significantly as the amounts scale up. For instance, it would mean losing 100,000 TZS for $1,000 and a million for $10,000. These aren’t just small, forgettable amounts—they’re chunks that would otherwise serve as a buffer against inflation and currency devaluation. In the bigger picture, these “pennies” add up quickly, often costing us a significant portion of our hard-earned money that could be better protected and grown on-chain.

L2s Scaling Cost-Efficiency and Enabling a Decentralized Future

Touted as a financial system built with people in mind, DeFi anchors on the core principle of putting power back in the hands of the people. With DeFi, you can trade and transfer value peer-to-peer, with no intermediaries—no banks or governments in between trying to siphon off fees and taxes. In the end, you have a low-cost, faster, and more secure way of moving money, unlike traditional systems like banks, mobile money, or SWIFT.

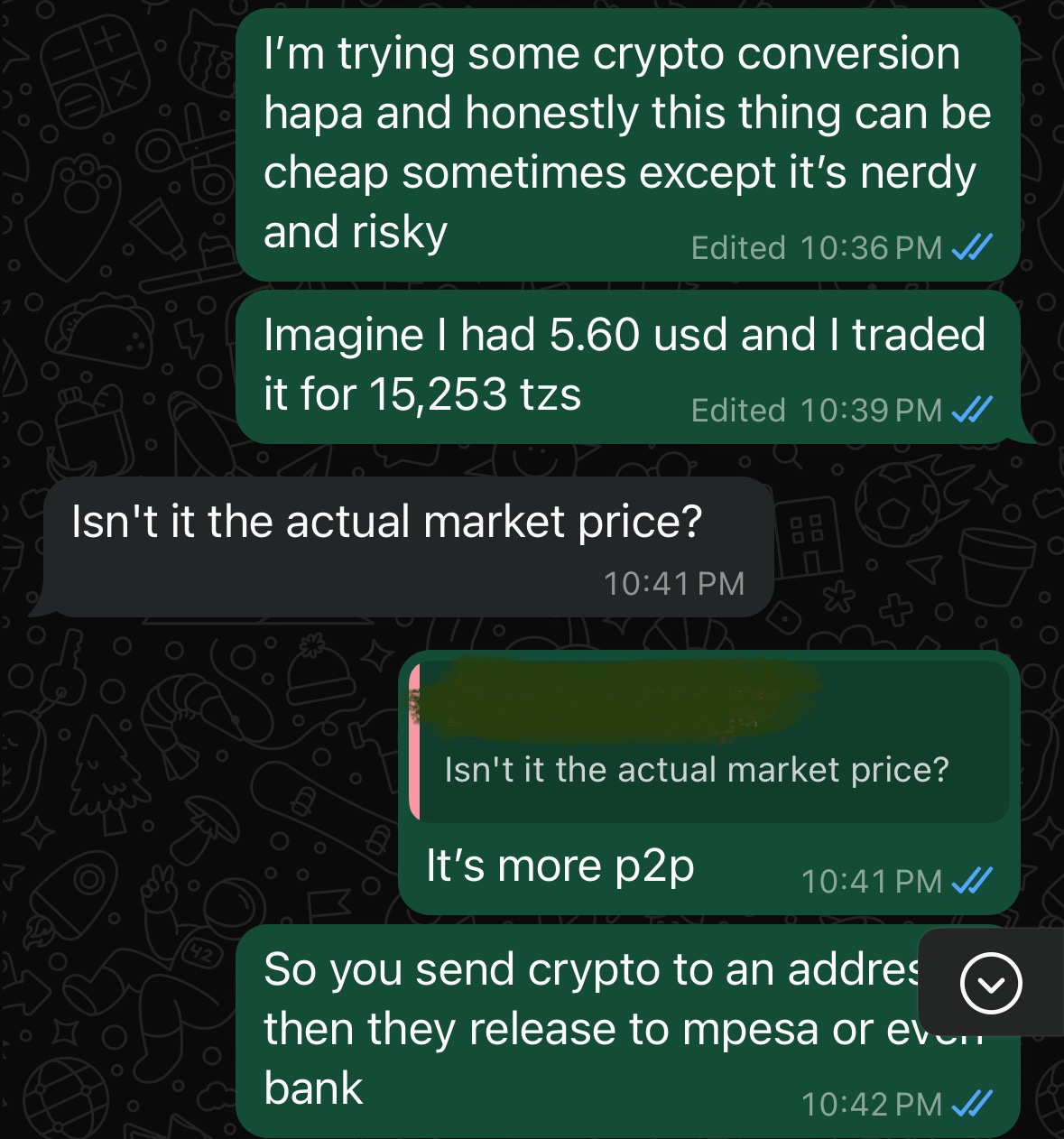

Gone are the days of longer transaction validation, higher gas fees (transaction costs), and slower transactions due to network congestion on chains like Ethereum and BTC. Advances in Layer 2 scaling solutions, or side chains like Base on the Ethereum network, have slashed transaction costs and removed barriers that previously stopped many from realizing the full power of on-chain money. Now, more than ever, you can move money globally at an incredibly cheap cost, and the person on the other end can withdraw easily by converting digital dollars to cash through peer-to-peer transactions, negotiating rates to get even more value.

In my recent experience, I converted a few USDT in my wallet at a rate of 2740, and to my surprise, I got a slightly higher rate than what Google reported for USD to TZS that day.

Of course, some might argue that the on-chain ecosystem is too technical to grasp. It’s true. But over time, so much has become simplified—even for your grandma to understand. And if you’re conscious about making the most of your money, perhaps you shouldn’t ignore the wealth-creation opportunities that DeFi unlocks.

Just imagine the convenience and benefits of saving in USD, along with the flexibility and composability of doing what you want with your money. Imagine a fairer peer-to-peer-driven way to transfer and share value through chains like Base, and finally, a fairer P2P market enabling swift conversion of your digital dollars back to fiat—without the hassle of hunting for a bank or worrying about bank fees. That’s the promise of DeFi and crypto, and it’s why you should consider banking on-chain.

Leave a Reply